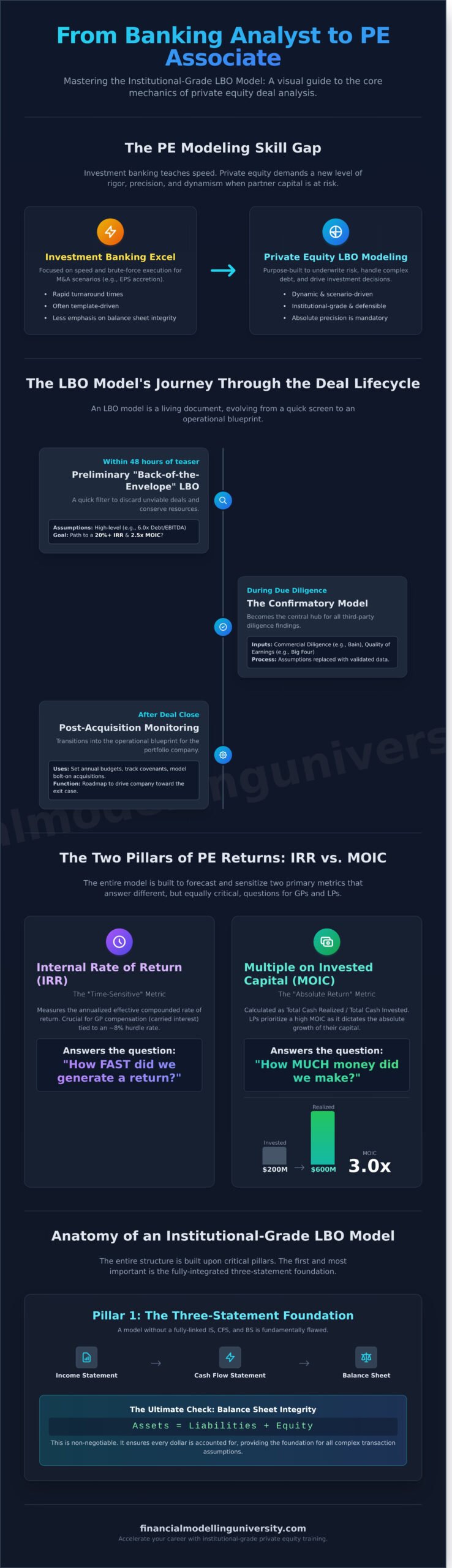

Your investment banking Excel skills are nearly irrelevant in a top-quartile private equity fund. It’s a harsh reality. While your banking analyst stint taught you speed and brute-force Excel, it likely never forced you to build the dynamic, institutional-grade models that drive real investment decisions. The stakes are simply different when partner capital is on the line, and the fear of a flawed model tanking a deal presentation is a constant pressure.

This guide demystifies the sophisticated mechanics of private equity financial modeling. You will move beyond simplistic templates to master the complex debt schedules, dynamic operating scenarios, and precise return calculations, like IRR and MOIC, that separate top-tier candidates from the rest of the pack. We will walk you through building a robust, deal-ready LBO model from a blank Excel sheet, giving you the technical firepower to ace the modeling test and defend your investment thesis with conviction.

Key Takeaways

- Understand how LBO models evolve from initial screening to final due diligence, enabling you to add value at every stage of the deal lifecycle.

- Master the three-statement foundation of an institutional-grade LBO, ensuring the balance sheet integrity required for complex transaction assumptions.

- Go beyond traditional Excel by learning how AI-augmented workflows are revolutionizing private equity financial modeling for faster, more accurate scenario analysis.

- Learn the critical first steps to building a robust LBO model, from cleaning historical data to structuring the definitive Sources and Uses table.

The Role of Private Equity Financial Modeling in the Deal Lifecycle

In the high-stakes world of leveraged buyouts, private equity financial modeling is not a technical exercise; it is the core discipline for quantifying risk and underwriting returns. An institutional-grade LBO model is the crucible where an investment thesis is forged. Unlike a standard corporate M&A model focused on EPS accretion for a strategic buyer, the LBO model is purpose-built for a financial sponsor. It must dynamically handle complex capital structures, model operational value creation levers, and sensitize returns across multiple exit scenarios. For a more general Financial Modeling Overview, the fundamental principles of forecasting are shared, but the application in PE is a specialized and far more rigorous craft.

From Deal Sourcing to Final Investment Committee

A private equity deal model is not a static document; it is a living repository of knowledge that evolves in complexity and precision throughout the deal lifecycle. It begins as a rapid screening tool and culminates in the definitive document underpinning a nine-figure investment decision. This evolution typically follows three distinct phases:

- Preliminary Modeling: Within 48 hours of receiving a teaser, an analyst builds a “back-of-the-envelope” LBO. Using high-level assumptions, such as a 6.0x Debt/EBITDA entry multiple and a 2.0% annual margin expansion, this initial pass serves as a quick filter. If a path to a 20%+ IRR and a 2.5x MOIC isn’t immediately apparent, the deal is often discarded, saving thousands of hours in wasted diligence.

- The Confirmatory Phase: Once a deal progresses, the model becomes the central hub for all third-party due diligence. Projections from a commercial diligence report by Bain & Company are used to build the revenue forecast. The Quality of Earnings adjustments from a Big Four accounting firm are hard-coded to establish a defensible baseline EBITDA. The model’s assumptions are systematically replaced with validated data.

- Post-Acquisition Monitoring: After the deal closes, the final LBO model becomes the operational blueprint for the portfolio company. It is used to set annual budgets, track covenant compliance, and model strategic initiatives like a bolt-on acquisition or a dividend recapitalization. It is the roadmap used to drive the company toward the exit forecasted in the original investment case.

Key Metrics: IRR vs. MOIC

Ultimately, the entire private equity financial modeling process is designed to forecast and sensitize two primary return metrics that the Investment Committee cares about. While they are related, they answer two fundamentally different questions and are critical for aligning the interests of the General Partners (GPs) and their Limited Partners (LPs).

The Internal Rate of Return (IRR) is the time-sensitive metric. It measures the annualized effective compounded rate of return. GPs are compensated via carried interest, which is typically contingent on clearing an 8% preferred return, or “hurdle rate.” Therefore, generating strong returns quickly has a direct impact on their compensation. It answers the question, “How fast did we generate a return?”

Conversely, the Multiple of Invested Capital (MOIC), or cash-on-cash return, is the absolute return metric. It’s calculated by dividing the total cash realized by the total cash invested. If a fund invests $200M and receives $600M upon exit, the MOIC is 3.0x. LPs, who commit capital for a fund’s 10-year life, often prioritize a high MOIC as it dictates the absolute growth of their initial investment. A robust model must also account for the “J-Curve” effect, where a fund’s net asset value is initially negative due to management fees and capital calls for new investments. The model’s cash flow timing is what makes it the single source of truth for the Investment Committee, providing a defensible projection of the entire investment journey from initial outlay to final exit.

Anatomy of an Institutional-Grade LBO Model

An institutional-grade LBO model is not a simple calculation; it’s a dynamic, multi-faceted tool engineered for precision and strategic decision-making. It’s the analytical backbone that separates a theoretical deal from an executable one. As detailed by Harvard Business School, The LBO Model is fundamentally a mechanism to assess the viability of an acquisition financed heavily with debt. The entire structure is built upon four critical pillars that every elite finance professional must master.

First is the Three-Statement Foundation. An LBO model without a fully integrated income statement, cash flow statement, and balance sheet is fundamentally flawed. Balance sheet integrity, where assets always equal liabilities plus equity, is non-negotiable. It’s the ultimate check that every dollar is accounted for, ensuring the model’s cash flows and capital structure are logically sound. A model that doesn’t balance is an immediate red flag in any deal process.

Next are the Transaction Assumptions. This is where the deal is born. Key inputs include:

- Entry Multiple: The purchase price is typically determined as a multiple of LTM EBITDA, for instance, 11.5x on $100 million of EBITDA implies a $1.15 billion Enterprise Value.

- Financing Mix: A typical structure might involve 65% debt and 35% sponsor equity. The debt itself is often layered, such as 4.5x EBITDA in Senior Secured Debt and 2.0x EBITDA in Unsecured Notes.

- Transaction & Financing Fees: These costs, often totaling 2.0% to 3.0% of the total transaction value, must be accurately modeled as they represent an immediate cash outflow and impact the initial balance sheet.

The third pillar is the Debt Schedules. This is the engine of the LBO, where the model’s sophistication truly shows. Each tranche of debt-be it Senior, Mezzanine, or a Unitranche facility-requires its own detailed schedule tracking interest payments, principal amortization, and the outstanding balance over the investment horizon. Effective private equity financial modeling demands this level of granularity.

Building the Robust Debt Schedule

A robust debt schedule meticulously models mandatory amortization alongside optional prepayments through a “Cash Sweep.” This mechanism uses a specified percentage, often 50% to 100%, of excess free cash flow to pay down outstanding debt ahead of schedule, accelerating deleveraging. The model must also track financial covenants, such as a maximum Net Debt / EBITDA ratio (e.g., not to exceed 6.0x) and a minimum Interest Coverage Ratio (e.g., must remain above 2.0x). Finally, it must account for PIK (Payment-in-Kind) interest, which accretes to the principal balance instead of being paid in cash, increasing the debt load at exit.

Finally, we model The Exit. The investment thesis culminates here. The exit is typically projected for Year 5, assuming an exit multiple on projected EBITDA (e.g., 12.0x). The real analytical power, however, comes from building sensitivity tables that display the Internal Rate of Return (IRR) and Multiple of Invested Capital (MOIC) across a range of exit multiples and holding periods. This demonstrates a clear understanding of risk and return drivers to an investment committee.

The Returns Waterfall

The “Waterfall” is the final distribution of exit proceeds among stakeholders, dictating precisely who gets paid, in what order, and how much. This model first allocates proceeds to repay all outstanding debt. The remaining equity value is then distributed, typically starting with a preferred return (e.g., an 8% annual return) to Limited Partners (LPs). Next, a catch-up provision often allows the General Partner (GP) to receive a disproportionate share of profits until it “catches up” to its 20% carried interest allocation. Finally, all remaining profits are split, usually 80/20 between LPs and the GP. Don’t forget the Management Incentive Plan (MIP), a 5-10% equity pool for the management team that dilutes the sponsor’s stake and must be factored into the final returns. Mastering the complexities of the returns waterfall is a core competency that distinguishes top-tier analysts. Our Advanced LBO Modeling course provides a step-by-step framework for building these dynamic structures.

Evolutionary Modeling: Traditional Excel vs. AI-Augmented Workflows

The landscape of private equity financial modeling is undergoing a tectonic shift. The era of the analyst spending 80% of their time on manual data entry from SEC filings is definitively over. Today’s elite deal teams leverage technology not to replace financial acumen, but to amplify it. This evolution separates the efficient, high-impact analyst from the one buried in legacy processes. The core challenge isn’t just learning new tools; it’s integrating them into a workflow that maintains institutional-grade precision and auditability.

This transition begins with data. Instead of manually keying in financials, analysts now deploy automated scripts and API connections to platforms like Capital IQ and FactSet, pulling and cleaning datasets in minutes, not days. A 2023 internal study at a major U.S. buyout fund revealed that integrating automated data feeds reduced initial data preparation time for a standard LBO model by an average of 40%. The next layer is execution. An analyst can now prompt a generative AI, like Microsoft 365 Copilot, to write a complex VBA macro for a multi-tranche debt waterfall or a Monte Carlo simulation with 10,000 iterations. This automates tasks that once required hours of specialized coding, freeing up critical time for higher-value analysis.

Yet, this power introduces a critical risk: the “black box” model. Relying on AI-generated code without a line-by-line audit is a career-ending mistake. Every formula, every cell reference, and every logical test must be transparent and defensible before an Investment Committee. A model you can’t explain is a model you don’t own. The barrier to entry in this field isn’t access to technology; it remains a deep, unshakable command of financial fundamentals. The tools get you to the answer faster, but they don’t tell you if the answer is right.

Tooling Up for 2026

For deal-specific LBOs, Excel remains the undisputed gold standard due to its flexibility and universal adoption. However, for portfolio-level analysis across dozens of operating companies, its limitations become apparent. Here, Python, with libraries like Pandas and Matplotlib, offers superior power for handling datasets exceeding Excel’s 1,048,576 row limit. While specialized PE software like DealCloud offers CRM and pipeline management, it can’t replicate the bespoke, granular modeling required for a high-stakes transaction.

The Human Element in High-Stakes Modeling

Technology can project future cash flows based on historical data, but it cannot interpret the “why” behind them. It can’t model the strategic impact of a new management team or the reputational risk of an ESG controversy. This is the domain of the analyst. Your role is to pressure-test the model against “Black Swan” events, modeling scenarios for macro volatility like the sudden credit market freeze of 2022. You are the essential bridge between raw data and investment intuition.

Step-by-Step: Building Your First Professional LBO Model

Theoretical knowledge separates you from the crowd. Flawless execution places you in the elite. Building an institutional-grade LBO model is a non-negotiable skill, a rigorous process that transforms an investment thesis into a dynamic, decision-making tool. The precision you demonstrate here directly reflects the quality of your thinking and your potential as a deal professional. Let’s move from concept to construction.

A professional LBO model is built with a logical, five-step sequence. Deviating from this structure introduces risk and inefficiency. Master the workflow.

- Step 1: Clean the historical data and build the 3-statement core. This is the foundation. You must scrub historical financials for non-recurring items and normalize accounting policies. From this clean base, you build a fully linked three-statement model that forms the engine for all future projections.

- Step 2: Define the transaction structure and “Sources and Uses” table. This table is the architectural blueprint for the entire deal. It outlines precisely where every dollar comes from and where it is allocated at close.

- Step 3: Forecast operations based on a specific investment thesis. Your projections are not random guesses. They are the financial translation of your value creation plan, whether it’s expanding into a new market, cutting SG&A by 150 basis points, or executing a roll-up strategy.

- Step 4: Layer in the debt and interest expense schedules. This is the heart of the LBO. You must model the debt tranches, interest calculations (including PIK interest), and the cash flow sweep mechanism that dictates how debt is paid down. This is the core discipline of private equity financial modeling.

- Step 5: Calculate exit returns and run sensitivity “football fields”. The final output. You calculate the sponsor’s IRR and Multiple on Invested Capital (MoIC) and then stress-test those returns against key variables to understand the deal’s risk profile.

The Sources and Uses Table

This table must balance to the penny. Every “Use” of cash, from the equity purchase price to transaction fees, must be funded by a “Source,” like sponsor equity or new debt. Key complexities include accounting for a minimum cash balance required to run the business post-close and refinancing the target’s existing debt. Critically, transaction advisory fees are typically capitalized into Goodwill, whereas financing fees are capitalized on the balance sheet and amortized over the life of the debt, impacting future net income.

Sensitivity Analysis and Stress Testing

The “Football Field” chart is the ultimate summary for an investment committee. It visualizes the range of potential IRR and MoIC outcomes based on key assumptions. Operating sensitivities might test a revenue growth CAGR of 5% versus 8%, while financial sensitivities reveal the impact of a 200 bps hike in SOFR on your returns. This robust analysis demonstrates you’ve considered every angle, a hallmark of superior private equity financial modeling.

Executing these steps with speed and accuracy is what separates a top-bucket analyst from the pack. It’s a technical craft that unlocks immense career leverage. Build models that win deals and secure your place at the table. Enroll in our Elite LBO Modeling Bootcamp to master the process from start to finish.

Accelerate Your Career with FMU’s Private Equity Training

Theoretical knowledge won’t secure you a seat at a top-tier private equity fund. The recruiting process is a deliberate gauntlet designed to identify candidates who possess not just academic understanding, but the practical, high-pressure execution skills of a seasoned analyst. It’s where most aspiring professionals fail. At Financial Modelling University, we bridge this critical gap, moving you from theory to a state of complete deal-readiness.

Our curriculum is built on a library of over 50 real-world case studies, deconstructing actual transactions from the last 24 months. You won’t build generic models; you’ll replicate the complex capital structures and operational assumptions behind recent multi-billion dollar take-private LBOs. This focus on applied private equity financial modeling ensures you develop the dynamic, robust skills required on day one of the job. It’s a direct simulation of the deal team environment, engineered to forge institutional-grade competence.

The FMU University All-Access Pass is your complete arsenal. It provides a comprehensive progression from foundational three-statement modeling to the most complex LBO and M&A frameworks used at bulge-bracket banks and mega-funds. Upon mastering the curriculum, you earn a globally recognized certification that validates your elite modeling skills to recruiters, providing definitive proof that you can perform at the highest level.

A perfect model is useless if you can’t defend it. Our one-on-one career mentoring prepares you for the intense scrutiny of the technical interview. We drill you relentlessly on the “Paper LBO”-a critical test in over 85% of PE interviews-and dissect the nuanced questions that expose weak candidates. We ensure you can articulate the commercial logic behind every calculation, a skill that separates top 1% applicants from the rest.

The FMU Methodology: Expert Practitioner Insight

You learn directly from seasoned mentors who have managed deal teams and closed transactions exceeding $5 billion in enterprise value. This isn’t academic instruction; it’s an apprenticeship in professional excellence. You gain access to our library of downloadable Excel templates, the exact institutional-grade frameworks used by analysts at KKR, Blackstone, and Carlyle to evaluate live deals. Check our LBO Modeling Course for deep-dive tutorials on these elite techniques.

Securing the Offer

The 4-hour in-person modeling test is the final gatekeeper. We train you to execute with both speed and precision under extreme pressure, a non-negotiable requirement for success. You’ll master the workflows needed to avoid common mistakes that immediately disqualify over 90% of candidates, such as:

- Incorrect debt schedule logic and cash flow sweeps

- Flawed circularity toggles that break the model

- Illogical returns sensitivity analysis and IRR calculations

Don’t let a technical error stand between you and a career in private equity. Join the FMU University All-Access Pass today and master the craft.

Execute the Model, Secure the Offer

You’ve dissected the anatomy of an institutional-grade LBO and understand its critical role throughout the deal lifecycle. The difference between theory and execution, however, is what separates an applicant from an associate. The gap between knowing the steps and building a dynamic, error-proof model under the pressure of a 3-hour case study is where most candidates fail.

This is the precise challenge our curriculum is engineered to solve. Mastering private equity financial modeling with FMU means you’re not just learning; you’re replicating the exact workflows of elite funds. You get access to our complete suite of downloadable institutional-grade Excel templates, receive direct 1-on-1 mentoring from former bulge-bracket associates, and earn a globally recognized certification trusted by over 150 leading financial firms.

Stop preparing. Start performing.

Master the LBO and secure your Private Equity offer with FMU.

Frequently Asked Questions

What is the most important part of a private equity financial model?

The most critical component is the operating forecast, specifically the assumptions driving revenue growth, EBITDA margins, and capital expenditures. While the debt schedule and returns calculations are mechanically complex, they are outputs. The operating assumptions are the primary drivers of free cash flow, which dictates debt paydown capacity and the ultimate equity return. An elegant LBO model is worthless if its core business projections are indefensible; this is where deals are won or lost.

How long does it take to learn private equity modeling?

Achieving interview-ready proficiency typically requires 100 to 150 hours of dedicated, focused practice. This involves building multiple, dynamic LBO models from a blank Excel sheet to an institutional-grade final product. An experienced analyst can build a robust model in 4-6 hours; a candidate must replicate that speed and precision under pressure. The learning curve is steep, but mastering the mechanics is a non-negotiable prerequisite for any serious private equity candidate.

Do I need to know VBA for private equity modeling in 2026?

No, VBA is not a core requirement for over 95% of junior private equity roles. Your focus must be on mastering advanced Excel functions, including INDEX/MATCH, OFFSET, and data tables, which are essential for building dynamic and error-proof models. While VBA can automate certain tasks, firms prioritize candidates who demonstrate flawless command of core modeling logic and accounting principles. A robust, well-structured model built without macros is far more valuable than a fragile one that relies on them.

What is a “Paper LBO” and why is it used in interviews?

A Paper LBO is a simplified leveraged buyout analysis conducted without a computer, typically on paper or a whiteboard, during an interview. It’s designed to test your conceptual understanding of the key return drivers: entry and exit multiples, leverage levels (e.g., 6.0x EBITDA), and the company’s ability to generate cash to pay down debt. Interviewers use it to quickly assess if you can think critically about a deal’s structure and economics under pressure, separating candidates who understand the theory from those who can only follow a template.

How does an LBO model differ from a standard DCF?

The primary difference is the objective. An LBO model solves for the internal rate of return (IRR) for equity investors given a specific transaction structure, including a detailed debt schedule. A Discounted Cash Flow (DCF) model, in contrast, solves for a company’s intrinsic enterprise value by discounting its unlevered free cash flows at the weighted average cost of capital (WACC). An LBO is a financing-focused valuation tool from a sponsor’s perspective, while a DCF is a fundamental valuation method.

What are the most common mistakes in PE modeling tests?

The most frequent errors, accounting for over 70% of failures, are fundamental mechanical flaws, not high-level strategic misjudgments. These include an unbalanced balance sheet, incorrect linking of the cash flow statement to the debt schedule (the “cash flow sweep”), and miscalculation of transaction fees and financing fees in the Sources & Uses table. Another critical error is failing to build in a circularity switch, causing the model to crash. Precision on these granular details is what separates a pass from a fail.

Can I get a job in private equity without an MBA if I master modeling?

Yes, absolutely. For pre-MBA associate roles, elite technical skill is the primary gatekeeper, and the ability to build an institutional-grade LBO model from scratch is the most critical technical test. Top firms like Blackstone, KKR, and Carlyle consistently hire analysts directly from investment banking and other rigorous training grounds. Demonstrating deep modeling expertise signals you can execute the core job function from day one, often making you a more valuable hire than a candidate with an MBA but weaker technical skills.

How does the FMU certification help in the PE recruiting process?

The FMU certification serves as a powerful, third-party validation of your technical capabilities to recruiters and deal professionals. It acts as a credible signal that you have mastered the complexities of institutional-grade private equity financial modeling before you even enter the interview room. This de-risks the hiring process for firms, as it proves you’ve undergone rigorous training recognized by industry leaders. Possessing the certification can directly lead to securing more interviews and passing technical screening rounds with greater frequency.