Most professionals mistake commercial real estate development for a simple construction exercise, yet in the institutional world, it’s actually a rigorous process of manufacturing alpha through precise financial engineering. While a physical structure is the visible result, the real work happens within the capital stack and the entitlement phase. A 2023 study by the Urban Land Institute found that 68% of project failures stem from misaligned funding structures rather than actual site delays. To excel in this competitive market, you must move beyond the “bricks and mortar” mindset and adopt the perspective of a seasoned sponsor who views every square foot as a derivative of risk and return.

It’s understandable if you feel overwhelmed by the complexity of a four-year project timeline or the opaque nature of debt-to-equity transitions. You’ve likely realized that a basic spreadsheet won’t suffice when you’re managing a $150 million office or industrial build. This reference guide serves as your technical roadmap to mastering the lifecycle, financial mechanics, and strategic frameworks of large-scale projects. You’ll gain a granular understanding of the 5-stage development lifecycle and learn how elite developers manufacture value while mitigating downside risk. We’ll conclude by identifying the specific modeling competencies required to build the institutional-grade frameworks that top-tier private equity firms demand.

Key Takeaways

- Transition from passive investment to manufacturing value by mastering the strategic conversion of underutilized assets into institutional-grade property.

- Navigate the rigorous five-stage lifecycle of commercial real estate development, from initial site control and entitlements to final project execution.

- Deconstruct the complexity of the capital stack to effectively leverage senior debt, mezzanine financing, and preferred equity for maximum project viability.

- Execute precision-based feasibility analyses that stress-test market absorption rates and financial metrics against fluctuating interest rate environments.

- Utilize institutional-grade financial modeling to track the elite performance indicators-IRR, Equity Multiple, and Cash-on-Cash-that drive global investment decisions.

What is Commercial Real Estate Development in 2026?

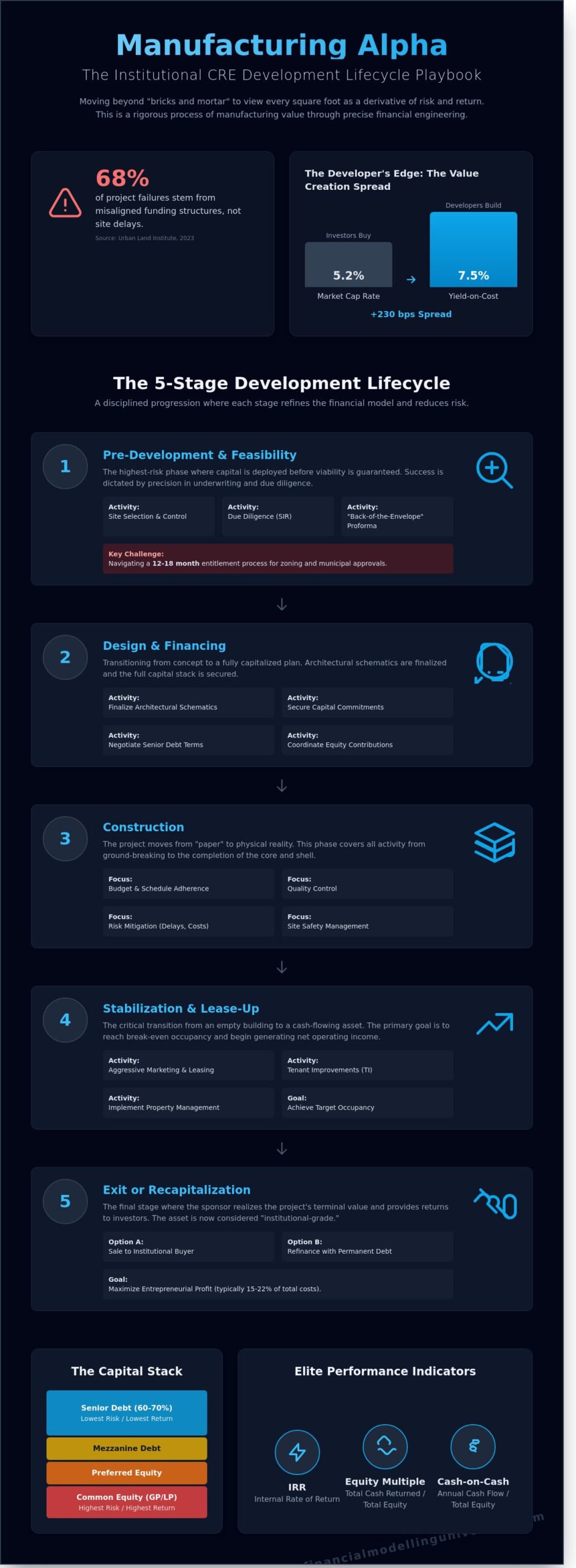

Commercial real estate development in 2026 is the industrial-scale manufacturing of value. It’s the process of converting raw land or underutilized assets into institutional-grade property through a rigorous cycle of planning and execution. While core investment focuses on acquiring existing cash flow, development focuses on creating it from zero. This distinction is critical for any serious analyst. Investors buy a 5.2% cap rate; developers build to a 7.5% yield. This 230-basis point spread represents the compensation for taking on entitlement, construction, and lease-up risk.

The real estate development process encompasses five core asset classes: industrial, multi-family, office, retail, and mixed-use. In the current market, industrial and multi-family dominate institutional allocations, often making up 68% of new construction starts. Development remains the highest risk-reward quadrant in the real estate universe. It demands technical precision and a tolerance for volatility that standard acquisition strategies don’t require.

The Value Creation Premise

Value isn’t found; it’s engineered. Developers manufacture alpha primarily through rezoning and densification, turning a single-story warehouse into a 20-story residential tower. This transformation drives the Entrepreneurial Profit, a line item in the proforma that typically targets 15% to 22% of total project costs. Commercial real estate development is a value-add strategy involving physical and legal transformation to achieve highest and best use. It’s the ultimate test of a firm’s underwriting accuracy and market timing.

Development vs. Acquisition Strategies

Choosing to build versus buy hinges on the spread between Yield-on-Cost (YoC) and the Market Cap Rate. When inventory is tight, as seen in the 4.1% vacancy rates of late 2024, institutional investors shift toward commercial real estate development to capture higher margins. The developer acts as the “Sponsor” or “General Partner” (GP), providing the execution expertise while limited partners provide the bulk of the capital. This structure aligns incentives, ensuring the GP delivers a robust, institutional-grade asset that meets the rigorous demands of global capital markets. Mastery of this spread is what separates elite practitioners from passive participants.

The 5 Stages of the Commercial Development Lifecycle

Successful execution in commercial real estate development requires a disciplined progression through five distinct phases. Each stage represents a shift in the risk profile and a tightening of the financial model.

This entire process is a masterclass in high-stakes project management, and professionals looking to formalize their skills in this area often seek out expert training from resources like woloyem.com.

- Step 1: Pre-Development: This involves site selection, securing site control through options, and conducting due diligence. It’s the highest-risk phase because capital is deployed before project viability is fully guaranteed.

- Step 2: Design and Financing: Developers finalize architectural schematics and secure the capital stack. This includes negotiating senior debt and coordinating equity contributions.

- Step 3: Construction: The project moves from “paper” to vertical reality. This stage spans from the initial ground-breaking to the completion of the shell and core.

- Step 4: Stabilization: Management focuses on leasing velocity, executing tenant improvements (TI), and beginning formal operations to reach a break-even occupancy.

- Step 5: Exit or Recapitalization: The sponsor realizes the project’s terminal value through a sale to an institutional buyer or transitions to long-term permanent financing.

Pre-Development: The “High-Risk” Phase

Precision during pre-development dictates the project’s ultimate IRR. Developers must utilize a Site Investigation Report (SIR) to identify environmental encumbrances or utility gaps that could derail a budget. In the 2026 regulatory environment, navigating the entitlement process requires a 12 to 18-month lead time for municipal approvals and zoning variances.

Before committing significant "hard money," elite practitioners use "Back-of-the-Envelope" math to test the project’s feasibility. This initial proforma must account for current market cap rates and construction costs. Adhering to the rigorous standards found in the commercial real estate lending handbook ensures the project aligns with institutional risk management expectations. If the math doesn’t support a 15% to 20% development yield, the project is discarded. Mastering these early-stage calculations is why many professionals choose to refine their underwriting skills through structured training.

Construction and Stabilization

The transition to construction shifts the focus to cost control and schedule adherence. Managing the General Contractor (GC) is vital to mitigate the 10% to 15% cost overruns that frequently plague complex commercial real estate development projects. Lenders typically won’t release the full debt amount without significant de-risking. Securing 40% to 60% pre-leasing is often a prerequisite for closing the construction loan.

The issuance of the Certificate of Occupancy (CO) marks a critical milestone. It validates that the structure meets all building codes and allows tenants to move in. This trigger often unlocks the final tranches of a loan and initiates the stabilization period. The goal is to reach 90% occupancy, at which point the asset is considered "stabilized" and ready for institutional disposition or a 10-year fixed-rate refinance. Once stabilized, the focus shifts to optimizing ongoing operations and maximizing NOI through institutional-grade real estate asset management strategies that can add 200 basis points to realized returns.

Risk Management and Feasibility Analysis

Successful commercial real estate development hinges on quantifying uncertainty before the first shovel hits the ground. You’ve got to move beyond surface demographics to analyze specific absorption rates and consumer demand. For example, if a submarket shows a 4.2% vacancy rate in Class A office space, your financial model must reflect the 18 to 24 months it might take to lease up 50,000 square feet. Political risk, often driven by NIMBYism, can stall a project for two years, significantly eroding your levered returns. Zoning changes aren’t just administrative hurdles; they’re binary risks that can render a site worthless if the density isn’t approved.

Construction risk remains a primary threat to project solvency. Projections for 2026 indicate a 12% increase in structural steel costs and a persistent 15% shortfall in skilled labor. These fluctuations can’t be ignored. If you don’t account for these variables in your pro forma, your contingency fund will be depleted before the core and shell are complete.

The Feasibility Study Framework

The foundation of an institutional-grade analysis is the “Highest and Best Use” (HBU) study. This process determines if a parcel is best suited for industrial, multifamily, or retail use based on what’s physically possible and maximally productive. Sensitivity analysis is your most powerful tool here. A mere 100-basis point hike in interest rates can drop your Debt Service Coverage Ratio (DSCR) below 1.20, effectively killing the project’s IRR. Feasibility is an iterative process, not a one-time check, requiring constant updates as market data shifts.

Mitigation Strategies for Institutional Developers

Elite developers use specific mechanisms to cap exposure and protect the capital stack:

- Guaranteed Maximum Price (GMP) Contracts: These shift the risk of material price volatility in 2026 from the developer to the general contractor.

- Performance Bonds: These ensure the project reaches completion even if the primary contractor faces insolvency.

- ESG Integration: Implementing robust environmental standards can lower the cost of capital by 15 to 25 basis points through specialized green financing.

Environmental insurance is another critical layer. It protects against “unknown unknowns” like soil contamination discovered during excavation. By layering these protections, you ensure the commercial real estate development remains a viable investment even when macro conditions deteriorate.

The Capital Stack: How Development Deals are Funded

The capital stack dictates the risk and return profile of any commercial real estate development. At the foundation sits senior debt, typically covering 50% to 65% of the total Loan-to-Cost (LTC). This layer provides the lowest cost of capital because the lender holds the first lien position. If the project fails, the senior lender is paid first from the asset’s liquidation. Above this, mezzanine debt or preferred equity fills the 15% to 20% gap that senior lenders refuse to fund. These instruments are expensive, often carrying interest rates between 12% and 18%, but they allow developers to maximize leverage without diluting their equity stake too early.

The top of the stack consists of equity, split between the Sponsor (GP) and Limited Partners (LP). The GP provides the “skin in the game,” usually 5% to 10% of the total equity requirement. Institutional LPs, such as pension funds or private equity firms, provide the remaining 90%. This structure ensures the developer remains incentivized to perform, as their capital is the first to be wiped out in a downside scenario.

Understanding GP/LP Structures

GP/LP structures rely on the “Waterfall” distribution to align interests. This mechanism dictates the order in which cash flow is distributed to partners. Developers earn a “Promote,” which is a disproportionate share of the profits after hitting specific Internal Rate of Return (IRR) hurdles. You can learn more about Real Estate Waterfall distributions to understand the mechanics of these calculations. Most institutional deals include a 7% to 9% Preferred Return for the LP. A catch-up provision follows, allowing the GP to receive 100% of the next available profits until they’ve reached a specific ratio relative to the LP’s return.

Construction Financing vs. Permanent Debt

Financing a commercial real estate development requires managing the transition from high-risk construction loans to stabilized permanent debt. Construction loans are floating-rate, often priced at 300 to 500 basis points over SOFR, and are structured as interest-only. This creates significant “Refinance Risk.” Once the building reaches 90% occupancy, the developer must secure a 10-year CMBS loan or life insurance company debt. Lenders require a minimum Debt Service Coverage Ratio (DSCR) of 1.25x for stabilized assets. If interest rates spike during the 24-month construction period, the project may not generate enough cash flow to support the permanent loan amount needed to pay off the construction lender.

Mastering the Financial Engine of Modern Development

Excel remains the undisputed champion for institutional-grade modeling in the world of commercial real estate development. While specialized platforms exist, they often lack the transparency and flexibility required for rigorous due diligence. Institutional partners demand to see the logic behind every cell, making custom-built spreadsheets the industry’s universal language. You aren’t just calculating numbers; you’re stress-testing a vision against market volatility. Modern underwriting has moved past static, one-page proformas. It now requires dynamic multi-year models where every assumption, from terminal cap rates to construction cost escalations, is live and interactive.

Top-tier firms prioritize three core metrics to evaluate project viability:

- Internal Rate of Return (IRR): The primary measure of time-weighted profitability, typically targeted at 18% or higher for opportunistic projects.

- Equity Multiple: A measure of absolute wealth creation. An 18% IRR is less impressive if the Equity Multiple is only 1.2x over a short hold.

- Cash-on-Cash (CoC): This dictates the project’s ability to service debt and provide distributions once the asset stabilizes.

Once a development project reaches stabilization, the focus shifts from construction execution to maximizing operational performance through sophisticated real estate asset management techniques that can drive an additional 200 basis points in realized returns through precise lease optimization and capital allocation strategies.

The Skills Required for Institutional Development

Precision in development budgeting is non-negotiable. You must manage complex draw schedules where interest is capitalized and debt is layered in tranches. Modeling lease-up scenarios requires accounting for free rent periods and tenant inducements, which can erode net effective rent by 12% to 15% in competitive urban markets. Analysts now also face the rising demand for “Green” financing models. Integrating PACE financing or LEED-based interest rate reductions into a DCF is a specialized skill that separates elite practitioners from the pack.

Accelerating Your Career in CRE Development

The 2026 market will be defined by data-driven precision rather than gut feeling. Investment committees are purging generalists in favor of specialists who can navigate technical complexity with speed. Obtaining a certification in Real Estate Financial Modeling is no longer optional; it’s the price of admission for private equity firms and top-tier commercial real estate development shops. Technical mastery bridges the gap between theoretical knowledge and the high-stakes execution required to protect investor capital. To secure your position at the top of the field, join the FMU All-Access Pass to master professional real estate modeling.

Scaling Institutional Excellence in 2026

Success in commercial real estate development requires a granular mastery of the five-stage lifecycle and complex capital stack structures. Navigating 25% volatility in construction costs or securing 70% LTC financing requires a robust financial engine. You’ve analyzed the feasibility frameworks and the shifting debt-to-equity ratios that define modern projects. Precision underwriting is the only safeguard against market shifts. To lead a $50 million development project, you must bridge the gap between theoretical knowledge and elite execution. You can’t afford to guess on your next DCF or LBO model. Master Institutional-Grade Real Estate Modeling with FMU to access 15+ downloadable institutional-grade Excel templates and receive direct mentoring from former PE and IB practitioners. This globally recognized certification proves you can handle the high-stakes pressure of global finance. The market rewards those who treat every basis point with the respect it deserves. Start building your professional legacy today.

Frequently Asked Questions

What is the average profit margin for commercial real estate development?

Profit margins for institutional-grade commercial real estate development typically range from 15% to 25% of total development costs. You’ll target a 20% margin to account for market volatility and construction contingencies. This buffer ensures the project remains viable even if material costs rise by 5% during the build phase. Professional developers use these margins to justify the risk of capital to their equity partners.

How do I start a career in commercial real estate development with no money?

You start a career in commercial real estate development with no capital by securing an analyst role at a firm or leveraging a sweat equity partnership. 85% of successful developers began as analysts earning $85,000 to $120,000 annually. This path allows you to master the technical modeling skills required to manage multi-million dollar capital stacks. You’re building intellectual capital before you deploy your own financial capital.

What is the difference between a residential and a commercial developer?

The primary difference lies in the lease structure and the scale of the physical asset. Commercial developers focus on long-term 10 year leases with corporate entities, while residential developers manage 12 month leases with individuals. Commercial projects require complex debt structures like CMBS loans. These aren’t typically used in the residential 1 to 4 unit market, where financing relies on personal credit and standard mortgages.

What are entitlements in the context of land development?

Entitlements are legal approvals from local government agencies that grant you the right to develop a specific project. This process includes obtaining zoning variances, site plan approvals, and environmental permits. In high-demand markets like Austin or Miami, the entitlement phase often takes 18 to 24 months before you can break ground. Without these approvals, your land remains a speculative asset with limited institutional value.

How do interest rate hikes affect development feasibility in 2026?

Interest rate hikes in 2026 will likely force developers to maintain a minimum Debt Service Coverage Ratio of 1.30x to secure financing. If the Federal Funds Rate stays above 4.25%, your cost of capital increases, which directly compresses your yield on cost. You must model these scenarios with 50 to 100 basis point stress tests. This ensures the project doesn’t fail during the construction loan term.

What is a “Promote” in a real estate development deal?

A promote is a disproportionate share of profits paid to the General Partner once the Limited Partners achieve a specific return hurdle. In a standard institutional deal, the GP might receive a 20% promote after the investors reach an 8% Internal Rate of Return. This mechanism incentivizes the developer to exceed performance benchmarks through rigorous asset management. It’s the primary way developers build significant wealth in private equity.

Is an MBA necessary to become a commercial real estate developer?

An MBA isn’t necessary if you possess elite technical skills and a robust professional network. Data shows that 60% of hiring managers at private equity firms prioritize advanced financial modeling proficiency over a graduate degree. Saving the $200,000 cost of an MBA allows you to invest that capital into your first small-scale project. Mastery of the numbers is what creates professional authority in this field.

How long does a typical commercial development project take to complete?

A typical project takes between 3 and 5 years to move from land acquisition to stabilization. The first 12 to 18 months are dedicated to entitlements and design, while construction usually requires 18 to 24 months. You’ll then need an additional 6 to 12 months to reach 90% occupancy and secure permanent financing. Precision in your timeline modeling is critical to avoid expensive carrying costs on your debt.

One Response