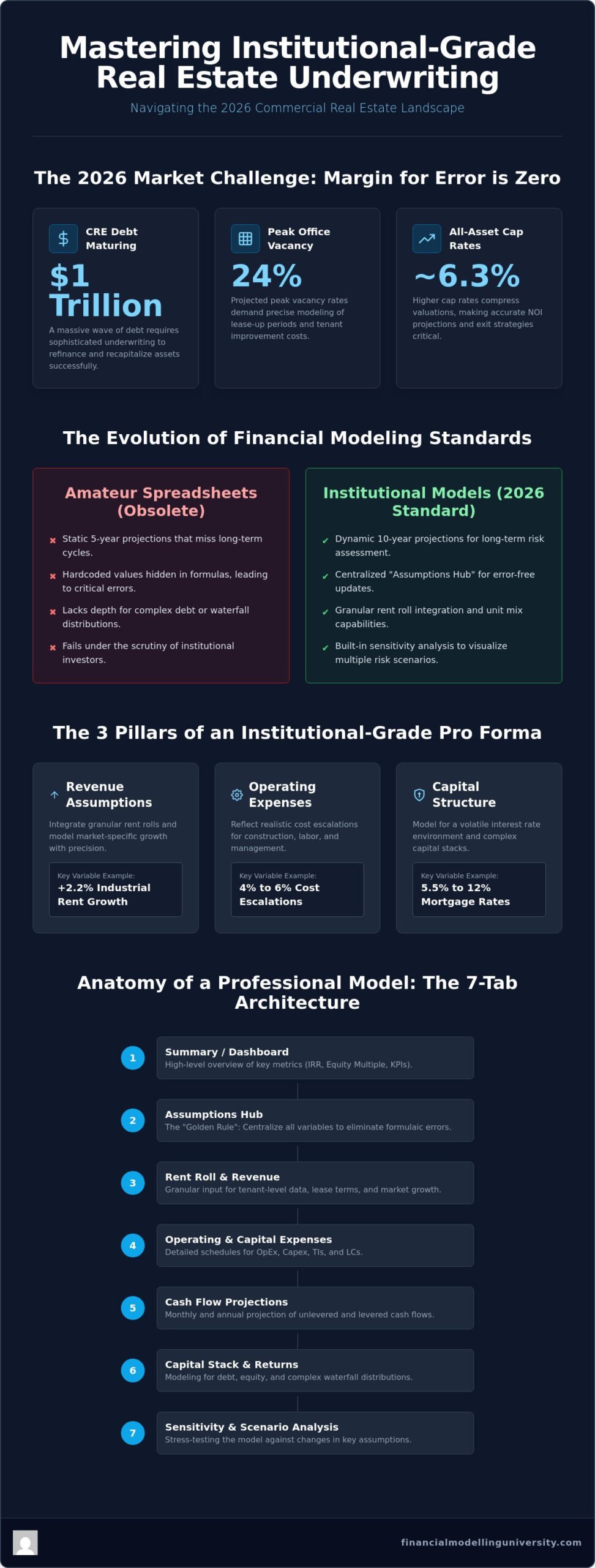

With roughly $1 trillion in commercial real estate debt maturing in 2026, the margin for error in your underwriting has effectively vanished. You’ve likely felt the frustration of downloading a “professional” model only to find it lacks the depth for complex debt structures or nuanced waterfall distributions. In a market where office vacancy rates are projected to peak at 24% and all-asset cap rates sit near 6.3%, an amateur spreadsheet is a liability you can’t afford.

At Financial Modelling University, we believe your tools should match your ambition. You’re about to master the architecture of institutional-grade underwriting and secure a professional real estate pro forma template excel built for the 2026 economic landscape. This isn’t just about inputting data; it’s about building a dynamic risk-mitigation engine that stands up to the scrutiny of elite investors and institutional partners.

We’ll guide you through the 2026 standards for CRE underwriting, from modeling persistent construction inflation to customizing frameworks for diverse asset classes. It’s time to stop second-guessing your formulas and start modeling with the precision and discipline of an industry expert. This guide provides the blueprint for your professional transformation.

Key Takeaways

- Transition from static 5-year projections to dynamic 10-year institutional models to meet 2026 market standards.

- Implement the “Golden Rule” of financial modeling by centralizing all variables in an Assumptions Hub to eliminate formulaic errors.

- Download and customize an institutional-grade real estate pro forma template excel designed to handle granular rent rolls and unit mix integrations.

- Leverage advanced Excel techniques like sensitivity tables and INDEX/MATCH logic to visualize multiple risk scenarios simultaneously.

- Master the communication strategies required to present your complex model effectively to private equity partners and investment committees.

What is a Real Estate Pro Forma? Defining the Institutional Standard

In the high-stakes environment of commercial real estate (CRE), a pro forma is more than a simple spreadsheet. It is a predictive financial model that serves as the numerical narrative for an investment’s lifecycle. While amateur investors might view it as a basic income statement, institutional practitioners treat it as a dynamic risk-assessment engine. This document utilizes the income approach to value to determine whether a property meets the rigorous internal rate of return (IRR) thresholds of elite funds. It’s the primary tool used to justify multi-million dollar capital allocations.

By 2026, the industry standard has shifted. Static five-year projections are now considered obsolete by major players. Top-tier firms demand dynamic 10-year models to account for the $1 trillion in CRE debt maturing this year and the prolonged stabilization periods seen in the office sector. Using a robust real estate pro forma template excel allows you to project these extended horizons with precision. At FMU, we’ve observed that the most successful analysts prioritize model integrity over simple aesthetics. Firms like Blackstone and J.P. Morgan don’t care about “pretty” tabs if a single broken link destroys the credibility of a $500 million deal.

Institutional-grade models rest on three non-negotiable pillars:

- Revenue Assumptions: These must integrate granular rent rolls and forecasted growth, such as the +2.2% industrial rent growth expected through 2027.

- Operating Expenses (OpEx): Models must reflect the 4% to 6% baseline construction and labor cost escalations currently hitting the market.

- Capital Structure: You must account for a volatile interest rate environment where commercial mortgage rates can swing from 5.50% to over 12% depending on borrower qualifications.

Pro Forma vs. Actuals: Managing the Variance

The gap between “as-underwritten” and “as-realized” is where professional reputations are made or lost. Managing variance isn’t just about tracking differences; it’s about understanding the “why” behind the numbers. Institutional models build in “actuals” tabs that feed back into the projection engine. This allows for real-time adjustments to exit cap rates and cash flow forecasts when market conditions, like the 18.6% office vacancy seen in early 2026, deviate from your initial thesis. It’s about being proactive rather than reactive.

Why Excel Remains the Industry Standard for CRE Underwriting

Proprietary software exists, but Excel remains the undisputed king of CRE. It offers a level of transparency that “black-box” platforms cannot match. A high-quality real estate pro forma template excel provides the flexibility to audit every cell, ensuring your logic is bulletproof before you step into the boardroom. In the world of elite finance, if you can’t show the formula, the numbers don’t exist. Excel allows for the bespoke logic required in complex joint ventures and tiered waterfall distributions that standard software often fails to handle.

Anatomy of an Institutional-Grade Real Estate Excel Template

Amateur models are often a graveyard of hardcoded numbers. In the institutional world, this is a fatal flaw. The foundational law of any professional real estate pro forma template excel is absolute transparency. You must never hardcode values within your calculation tabs. Every variable, from a 5.50% commercial mortgage rate to a 2.2% industrial rent growth forecast, must flow from a centralized Assumptions Hub. This architecture ensures that when you toggle a single input, the entire model updates instantly without breaking a formula or hiding a manual entry.

A professional model isn’t just about the final IRR. It’s about the logic that leads there. With $1 trillion in commercial real estate debt maturing in 2026, your model must handle complex refinancing scenarios and tiered capital stacks with surgical precision. If you want to perform at the level of elite practitioners, you can’t rely on simplified spreadsheets that gloss over mezzanine debt or construction loan draws. You need a framework that mirrors the complexity of a high-stakes deal.

The 7-Tab Architecture: From Inputs to Returns

Institutional models typically follow a logical, linear flow across seven core tabs. This structure starts with a high-level Dashboard for executives, followed by the Assumptions Hub and the granular Rent Roll. The engine room consists of the Operating Expenses (OpEx) and Debt Schedule tabs, which feed into the Cash Flow statement. Finally, the Waterfall tab handles equity distributions. This modular approach allows for rapid auditing and prevents the “spaghetti logic” common in inferior templates. You can master these complex structures in our Real Estate Financial Modeling Course.

Revenue Modeling: Base Rent, Recoveries, and Vacancy Loss

Revenue underwriting in 2026 requires more than a simple growth percentage. With office vacancy rates hitting 18.6% in early 2026, your model must account for “downtime” between leases and specific tenant improvement (TI) allowances. A professional template distinguishes between base rent, expense recoveries, and miscellaneous income, then applies a vacancy factor that reflects current market volatility. This granularity allows you to stress-test how a peak vacancy of 24% would impact your debt service coverage ratio (DSCR).

Operating Expenses: Fixed vs. Variable Costs in 2026

Inflation continues to squeeze margins, making accurate OpEx modeling vital. Your template should separate fixed costs, like property taxes (averaging 0.99% nationally), from variable costs like utilities and management fees. Given that construction labor costs have risen over 4% year-over-year, your model must include escalation factors for repairs and maintenance. Precise expense modeling prevents the “margin creep” that can turn a stabilized 6.3% cap rate acquisition into a cash-flow-negative disaster.

The final piece of the institutional puzzle is the Waterfall. This tab calculates the distribution of cash flow between the General Partner (GP) and Limited Partners (LP) based on specific IRR hurdles. It’s where the “promote” is calculated, and it’s often the most scrutinized tab in the entire workbook. Accuracy here is non-negotiable.

Step-by-Step: Building Your Pro Forma Template in Excel

Constructing an institutional-grade model requires a disciplined, sequential approach. You aren’t just linking cells; you’re building a logical framework that must withstand intense due diligence. Follow these steps to ensure your real estate pro forma template excel functions as a reliable decision-making tool.

Step 1: Property-Level Assumptions. Start by centralizing your global drivers. In 2026, your model must account for persistent inflation. Input a baseline construction cost escalation of 4% to 6% and reflect the national average property tax rate of 0.99%. These inputs will drive your entire forecast.

Step 2: Unit Mix and Rent Roll. Build a granular schedule that tracks every tenant or unit type. Don’t just project a lump sum. Integrate specific lease start and end dates to calculate “lost to lease” and downtime accurately. This level of detail is what separates a professional model from an amateur projection.

Step 3: Calculating NOI and ‘Below the Line’ Items. Subtract operating expenses from your effective gross income to find your Net Operating Income. Below the NOI line, account for Capital Expenditures (CapEx) and replacement reserves. These items impact your cash flow but don’t affect property valuation directly.

Step 4: Layering the Capital Stack. Integrate your debt schedule. With commercial mortgage rates starting around 5.50% for multifamily assets, you must model the specific interest rate, amortization, and loan-to-value (LTV) constraints. Calculate both Levered and Unlevered IRR to understand the true impact of your financing strategy.

Step 5: Implementing the Sensitivity Matrix. Create a data table that varies your exit cap rate and purchase price. In a market where all-asset cap rates hover near 6.3%, seeing how a 50-basis point shift affects your returns is critical for risk mitigation.

Calculating Net Operating Income (NOI): The Lifeblood of the Deal

NOI is the primary metric used to determine property value via the income approach. It represents the income generated after all operating expenses are paid but before debt service and taxes. Institutional investors focus on “stabilized NOI” to strip away temporary market fluctuations and assess the long-term health of the asset. If your NOI calculation is flawed, your entire valuation will be incorrect.

Modeling Capital Expenditures (CapEx) and Replacement Reserves

CapEx is often overlooked in basic models, leading to inflated return projections. In 2026, material costs are volatile. Copper is up 29.5% and aluminum has risen 45.3% year-over-year. Your real estate pro forma template excel must include a robust CapEx schedule to account for roof replacements, HVAC upgrades, and tenant improvements. Neglecting these “below the line” costs will result in a cash-flow shortfall that could jeopardize the entire investment.

Unlevered vs. Levered Returns: Understanding the Impact of Debt

Unlevered returns show the property’s performance as if it were purchased with 100% cash. Levered returns show the impact of using debt to “juice” the equity yield. While leverage can amplify gains, it also increases risk, especially in a high-interest environment. Professional analysts use the spread between the property’s cap rate and the mortgage interest rate to determine if the leverage is “positive” or “negative.”

Advanced Modeling: Sensitivity Analysis and VBA Integration

Static models are a relic of a low-volatility past. In 2026, an institutional-grade real estate pro forma template excel must act as a dynamic risk-mitigation engine. With national office vacancy rates projected to peak at 24%, your ability to visualize multiple outcomes simultaneously is a requirement, not a luxury. Elite practitioners don’t just present a single “likely” scenario; they stress-test every variable to ensure the deal survives market decompression.

Professional models utilize Excel Data Tables to create a Sensitivity Matrix, allowing you to map 25 or more variations of IRR and equity multiple in a single view. This isn’t an “additional item” as some suggest. It’s the core of the investment committee presentation. You must also account for the $1 trillion in maturing CRE debt by modeling interest rate hedges and floating rate debt scenarios. Without these advanced layers, your underwriting is incomplete.

Equity waterfalls in institutional deals often include complex ‘Catch-up’ and ‘Clawback’ provisions. These ensure that General Partners (GP) are rewarded for outperformance while protecting the Limited Partners’ (LP) capital. Your model must be flexible enough to handle these tiered distributions without breaking the logic flow. This level of precision is what separates a professional analyst from an amateur.

The Power of the Sensitivity Matrix: Exit Caps vs. Entry Prices

A sensitivity matrix provides a visual heatmap of your deal’s risk profile. By varying the exit cap rate, which averaged 6.3% across assets in early 2026, against your entry price, you can identify the exact “break-even” point for your equity. This allows you to demonstrate to partners exactly how much cap rate expansion the project can withstand before returns fall below your hurdle rates. It transforms a guess into a calculated strategy.

Introduction to VBA for Real Estate Model Automation

VBA is the secret weapon of high-output analysts. It isn’t about complexity; it’s about eliminating manual error and increasing speed. Use simple macros to automate scenario toggles between Base, Upside, and Downside cases. Instead of manually updating dozens of assumptions, a single button can re-calculate the entire model across different macro environments. You can master these professional automation techniques in our VBA for Financial Modeling Course.

Error Checking and Circular Reference Management in CRE Models

Institutional models must be bulletproof. Implement a dedicated “Checks” tab to monitor for circular references and formulaic inconsistencies. Use conditional formatting to trigger “Red Flag” alerts if the model becomes unbalanced or if a DSCR falls below lender requirements. If your model contains a hidden error during a high-stakes deal, your professional credibility is gone. A professional template includes built-in audit trails to ensure every calculation is verifiable.

From Spreadsheet to Career: Mastering REFM with FMU

Possessing an institutional-grade real estate pro forma template excel is only 10% of the battle. The remaining 90% of your value as an analyst comes from mastering the underlying logic and being able to defend every assumption under the heat of a partner’s scrutiny. In the competitive 2026 market, where $1 trillion in debt is maturing and office vacancies are peaking at 24%, firms aren’t looking for people who can fill in blanks. They want professionals who can build, audit, and pivot complex models in real time.

The FMU approach is designed to transform you from a template user into an architect of financial truth. We don’t just hand you a finished file; we teach you to build institutional-grade models from a blank sheet. This “blank sheet” discipline ensures you understand the mechanical flow between the rent roll, the debt schedule, and the equity waterfall. When you sit before an Investment Committee, you won’t just present numbers. You’ll present a bulletproof investment thesis backed by technical mastery.

Mastering these skills is the fastest catalyst for career transformation. Whether you’re aiming for a role at JP Morgan or an elite private equity shop, your ability to model complex deals is your primary currency. The precision you demonstrate in your real estate pro forma template excel reflects your professional discipline. It signals that you’re ready to perform at the level of the industry’s top 1%.

The Real Estate Financial Modeling Course: Your Path to Mastery

Our Real Estate Financial Modeling Course is the blueprint for this transformation. We move beyond basic theory to tackle real-world scenarios, including 2026-specific drivers like persistent construction inflation and volatile interest rate environments. You’ll learn to handle tiered waterfall distributions and sensitivity analysis with the same rigor used by global investment banks. This isn’t just training; it’s a career-defining upgrade.

Certification and the Professional Edge in 2026

In a saturated job market, an FMU certification serves as a quantitative hallmark of your expertise. It tells recruiters and partners that you’ve been trained in proven methods trusted by the industry. As transaction volumes are expected to increase by 16% to $562 billion in 2026, the demand for elite underwriting talent has never been higher. Secure your edge by demonstrating you can handle the most complex capital stacks in the business.

Join 25,000+ Professionals Mastering Finance with FMU

You aren’t just taking a course; you’re joining an elite network. FMU is trusted by over 25,000 finance professionals who’ve used our curriculum to break into high-stakes roles and master the art of the deal. From investment banking to project finance, our graduates are the ones leading the industry forward. Stop using amateur tools and start modeling like the pros. Choose your path and begin your journey toward mastery today.

Master the Future of Real Estate Underwriting

The 2026 commercial real estate market doesn’t reward guesswork. With $1 trillion in debt maturing and office vacancies hitting record peaks, your underwriting must be surgical. You now understand the essential architecture of institutional models, moving beyond static spreadsheets to dynamic risk-mitigation engines that account for persistent inflation and volatile cap rates. Securing a professional real estate pro forma template excel is the foundation, but true mastery comes from building these frameworks from scratch and defending your logic in the boardroom.

Join 25,000+ finance professionals who trust FMU to elevate their careers. Our curriculum provides direct mentorship from industry experts who have closed over $1B in deals and includes the exact institutional-grade Excel templates used by elite firms. Stop relying on amateur tools that lack depth. Start modeling with the precision and confidence of a top-tier industry practitioner.

Enroll in the Real Estate Financial Modeling Course and Master the Pro Forma

The path to professional mastery is disciplined, logical, and highly structured. We’ve provided the blueprint for your advancement. Now, it’s time to execute.

Frequently Asked Questions

What is the most important formula in a real estate pro forma?

The Net Operating Income (NOI) calculation is the foundation of any institutional model because it determines property valuation via the income approach. You calculate it by subtracting all operating expenses from your effective gross income. This figure represents the property’s ability to generate cash flow before debt service. Professional analysts focus on stabilized NOI to strip away temporary market fluctuations and assess the long-term health of the asset.

How do I calculate the Internal Rate of Return (IRR) in Excel for real estate?

Use the =XIRR() function in Excel for the most accurate results in real estate modeling. This formula is superior to the standard IRR function because it accounts for the specific dates of cash flows rather than assuming equal annual periods. Simply select your range of cash flows and the corresponding dates to determine the annualized return. This precision is vital when modeling the irregular cash flows common in value-add or development projects.

What is the difference between an unlevered and a levered pro forma?

An unlevered pro forma evaluates the property’s performance based solely on its cash-flow-generating potential, assuming a 100% cash purchase. This metric allows you to compare assets without the noise of different financing structures. A levered pro forma incorporates the capital stack, including senior debt and mezzanine financing. This distinction is critical because it shows how debt amplifies your equity returns or increases your risk in a high-interest environment.

How do I model a value-add real estate project in Excel?

Modeling a value-add project requires a granular Capital Expenditures (CapEx) schedule and a phased rent-increase assumption. You must account for the downtime during renovations and the subsequent “rent bump” once units are stabilized. Ensure your real estate pro forma template excel includes a construction draw schedule to track the timing of these improvements. This level of detail prevents cash-flow shortfalls during the critical renovation phase of the deal.

Should I use monthly or annual periods for my real estate pro forma?

Use monthly periods for the first 24 to 36 months of a deal, especially for development or heavy value-add projects. This captures the timing of construction draws and lease-up nuances that annual models miss. Transition to annual periods for the remaining holding period to maintain model efficiency. This hybrid approach provides the granular detail needed for stabilization while keeping the overall model clear for investment committee reviews.

What exit cap rate should I use in my 2026 real estate model?

Your exit cap rate should reflect current market conditions plus a conservative expansion buffer of 10 to 50 basis points depending on the asset class. With all-asset cap rates averaging 6.3% in early 2026, a 10-year exit might be modeled at 7.3% or higher. This conservative approach accounts for potential market decompression. It ensures your terminal value is realistic and not just a plug number used to juice the IRR.

How do I handle tenant improvements (TIs) and leasing commissions (LCs) in Excel?

Treat Tenant Improvements (TIs) and Leasing Commissions (LCs) as “below the line” capital items that reduce your net cash flow but do not affect your NOI. Build a dedicated leasing assumptions tab within your real estate pro forma template excel to track these costs on a per-square-foot basis. This ensures you account for the significant liquidity required to secure new tenants, which is essential given the 18.6% office vacancy rates seen in early 2026.